The firearms insurance market in the U.S. is facing challenges due to rising lawsuits and evolving regulations. Courts are narrowing what qualifies as an "accidental occurrence" under standard liability policies, leaving many firearms businesses without coverage for legal defense costs. Key developments include:

The combination of stricter court interpretations, new state laws, and higher insurance costs is forcing firearms companies to reassess their risk management strategies. Staying protected requires specialized insurance solutions and regular legal reviews.

Lawsuits are pushing insurers to rethink what their policies cover. At the heart of this shift is how courts define the term "occurrence" in liability policies. Traditionally, this term has referred to accidents or unforeseen events. However, recent legal decisions show that courts are increasingly siding with insurers, arguing that intentional actions don’t count as accidents. This evolving interpretation is reshaping how product liability, public nuisance claims, and other cases are handled by the courts.

Courts are now drawing a sharper line between accidental defects and intentional business decisions. For example, when a firearms company intentionally chooses specific marketing or sales strategies, any harm that results is often seen as a foreseeable outcome of those deliberate choices - not as an accidental event.

The Protection of Lawful Commerce in Arms Act (PLCAA) does have an exception for product defects, but applying this exception in insurance disputes has proven tricky. If harm stems from a criminal act - even if unintended - courts frequently view the criminal act as the "sole proximate cause." This interpretation can absolve the manufacturer of liability and leave insurers off the hook as well [4]. As a result, firearms businesses are finding product liability coverage less dependable.

States and cities are increasingly using public nuisance claims to sidestep federal protections. They argue that certain marketing and sales practices cause widespread harm to communities. Insurers, on the other hand, contend that these claims often seek government-related costs, like abatement, which aren’t typically covered by standard policies [1].

This strategy of using public nuisance claims to address societal problems, such as gun violence, mirrors approaches seen in opioid litigation. Adam Fleischer, an insurance-side partner at BatesCarey LLP, commented on this trend:

"The new wave of public nuisance suits generally present claims where a business scheme goes exactly according to plan - no accident exists; conduct remains intentional, and insurers won't cover planned actions" [1].

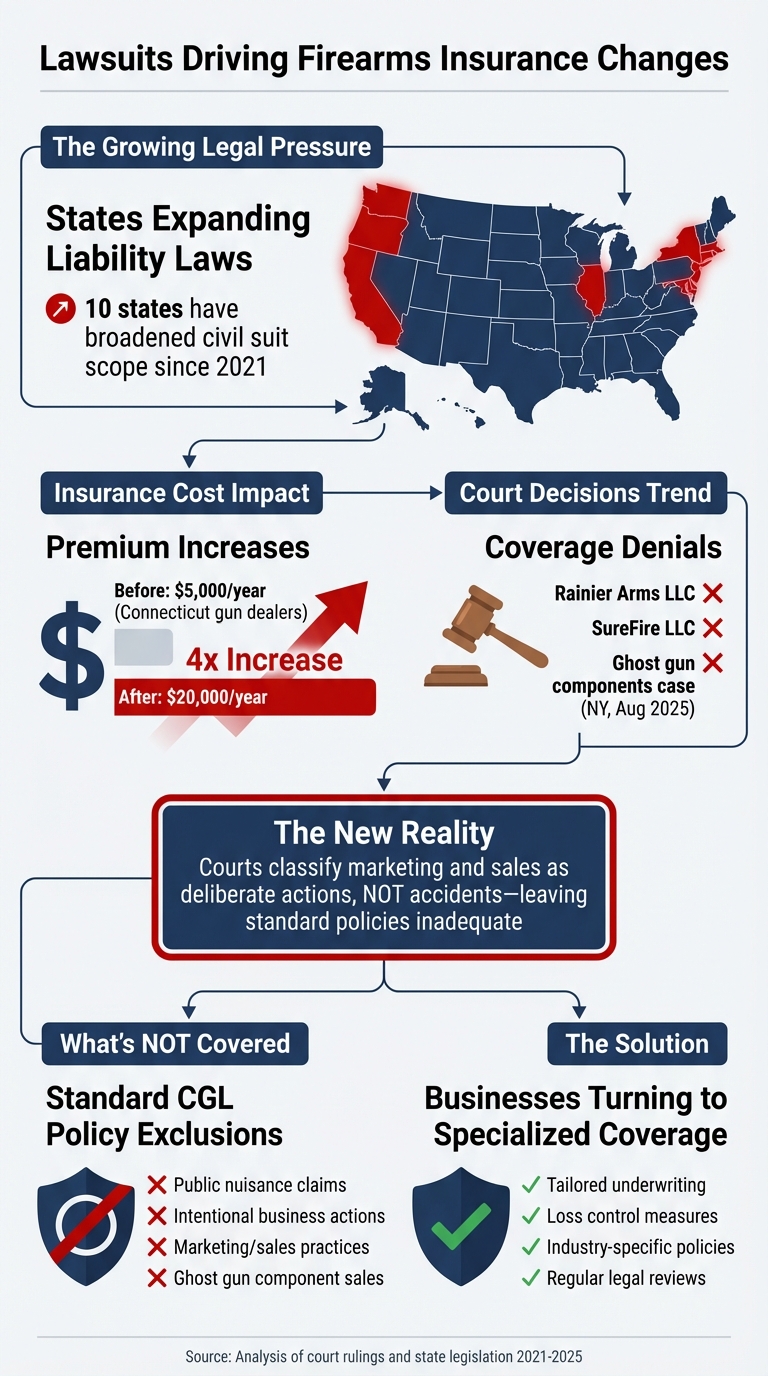

Recent court decisions, including cases involving Rainier Arms LLC and SureFire LLC, reinforce the idea that intentional business practices fall outside the scope of insurance coverage. Judges have consistently ruled that deliberate marketing and sales strategies do not meet the definition of accidental occurrences under standard liability policies [2][3].

Across the U.S., states are introducing new laws that push firearms businesses to reassess their insurance coverage. These laws bring unique challenges and responsibilities for those in the industry, adding to the shifting landscape of judicial rulings.

Connecticut has passed a law, set to take effect in October 2025, that allows lawsuits against gun manufacturers and retailers who fail to prevent firearms from ending up in the hands of unauthorized or high-risk individuals [11]. This law creates a legal obligation that standard insurance policies might not fully address.

Meanwhile, San Jose, California, has implemented a requirement for firearm owners to carry liability insurance to cover negligent or accidental firearm use. This coverage can be obtained through homeowners, renters, or specialized policies [9][10]. These evolving regulations are pushing firearms businesses to examine whether their current Commercial General Liability policies provide sufficient protection.

As these state mandates expand the responsibilities of the firearms industry, new legislative proposals are also raising the bar for insurance requirements.

Proposals in several states aim to enforce stricter insurance standards for firearms dealers, distributors, and manufacturers. These include mandates for higher minimum commercial liability coverage that extends to product-related and operational risks, as well as third-party injuries. Some proposed laws go further, requiring proof of insurance and imposing penalties for non-compliance.

In addition, certain bills suggest that business owners maintain coverage up to a specified minimum limit and allocate portions of insurance fees toward violence-prevention and victim-assistance programs. While many of these proposals are still under consideration, they point to a growing trend: firearms businesses may soon face stricter insurance requirements, including higher coverage limits and more specialized policies than what is typically seen today [7][9][10].

The surge in litigation is prompting insurers to rethink how they cover firearms businesses. Standard policies are being scrutinized, with higher costs and stricter terms becoming the norm. This shift has not only increased expenses but also pushed demand for customized insurance solutions.

Insurance carriers are responding to legal risks by hiking premiums and introducing exclusions to limit their exposure. For example, in Connecticut, the annual cost of gun dealer insurance has skyrocketed from $5,000 to $20,000 due to growing liability concerns [7]. Adding to this pressure are court decisions that deny coverage for public nuisance claims under standard Commercial General Liability (CGL) policies.

In a notable case from August 2025, a New York federal court ruled that AIG was not obligated to defend a firearms retailer involved in a lawsuit over "ghost gun" components. The court determined that selling such components without background checks constituted intentional actions, which fall outside the accidental events covered by CGL policies [19, 21]. Scott Seaman, Co-Chair of Hinshaw's Insurance Services Group, described this case as "well-traveled coverage territory", drawing parallels to opioid litigation where claims were denied due to the absence of bodily injury or qualifying damages [6].

To further limit their liability, insurers are now including exclusions for public nuisance claims and intentional acts, leaving firearms businesses to shoulder their own defense costs.

With standard policies falling short, firearms businesses are increasingly turning to specialized insurance solutions. Companies like Joseph Chiarello & Co., Inc., which has served the firearms industry for over four decades, provide coverage tailored to the unique risks these businesses face. Their offerings include Commercial General Liability, Firearms Business and Property Insurance, and Workers' Compensation, specifically designed for gun shops, shooting ranges, gunsmiths, wholesalers, and manufacturers [5].

These specialized policies go beyond basic coverage by incorporating features like employee background checks, loss control inspections, and underwriting that aligns with today’s legal landscape [5]. By addressing potential risks proactively, these solutions help firearms businesses stay protected as state laws continue to expand liability pathways.

With courts tightening coverage criteria and states ramping up liability laws, the firearms industry finds itself navigating a challenging and evolving risk environment. Since 2021, 10 states have broadened the scope for civil suits against firearm companies [12]. At the same time, courts have consistently denied coverage for public nuisance and ghost gun claims under standard Commercial General Liability (CGL) policies [6][8]. This combination of expanding legal exposure and shrinking traditional protections demands immediate attention.

For firearms business owners, staying ahead means focusing on risk management. Regular assessments and strict adherence to federal ATF requirements, state laws, and local regulations are critical. It’s worth noting that intentional acts remain outside the bounds of standard insurance coverage [6][8].

Traditional CGL policies no longer provide sufficient protection. Court rulings excluding public nuisance claims and intentional conduct highlight the need for specialized insurance. Businesses should seek out policies offering tailored underwriting, strong loss control measures, and efficient claims handling. Companies like Joseph Chiarello & Co., Inc. specialize in providing insurance solutions customized for firearms businesses across the United States.

Annual reviews with insurance and legal advisors are essential to ensure coverage aligns with shifting laws and court decisions. The cost of being unprepared far outweighs the investment in proactive risk management.

With litigation strategies increasingly aimed at financially destabilizing gun businesses [13], selecting the right insurance partner and maintaining comprehensive risk controls are no longer optional - they’re crucial for survival.

Recent court rulings are changing the landscape of firearms insurance, particularly by limiting coverage for lawsuits tied to claims like intentional marketing tactics or deliberate actions. This includes cases involving ghost guns or school shootings, which often don't align with the definition of an “occurrence” needed for coverage. In response, insurers are revising policy language and raising premiums to adapt to these legal shifts.

Companies like Joseph Chiarello & Co., Inc. are adjusting their policies to navigate these challenges while still offering customized insurance solutions for businesses in the firearms industry.

State laws are reshaping the insurance landscape for firearms manufacturers in notable ways. Take New York's 2021 public-nuisance law, for instance. This legislation requires gun manufacturers to adopt reasonable controls and opens the door for civil lawsuits if their products are used unlawfully. Meanwhile, New Hampshire has taken a different approach, passing a law designed to shield gunmakers from certain lawsuits. However, this protective measure is already facing its first legal challenges.

These legal shifts are forcing firearms manufacturers to reevaluate their insurance needs. As risks and liabilities vary across states, insurance policies are being adjusted to reflect these changes. For many businesses in the firearms industry, this could mean new coverage requirements and potentially higher premiums.

Firearms businesses are finding themselves in need of specialized insurance policies as lawsuits tied to ghost guns, school shootings, and other liability concerns continue to rise. These legal challenges have made it harder for traditional insurance plans to offer sufficient protection, leaving businesses vulnerable to major financial setbacks.

Specialized insurance policies cater specifically to the distinct risks these businesses face. They provide customized coverage to help shield against significant legal exposures, allowing companies to navigate the ever-changing legal and regulatory environment with more assurance.

Don't wait until it's too late to make sure your gun shop is covered. At Joseph Chiarello & Co., Inc., we’re here to help you navigate the ins and outs of gun shop workers compensation insurance to ensure you're prepared for any noise-related risks, including hearing damage. Reach out to us today to review your current policy or get a customized quote. Protect your team and your business with the right coverage—because their safety is worth it.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!