Misclassifying employees as independent contractors can lead to severe financial, legal, and operational risks for businesses. This issue is particularly pressing in industries like firearms, where safety and compliance are critical. Here's what you need to know:

To avoid these risks, businesses should conduct regular classification audits, follow clear criteria for worker classification, and partner with specialized insurance providers. Proper classification isn't just about compliance - it's about protecting workers and ensuring long-term business stability.

Employee misclassification in workers' compensation happens when workers are incorrectly labeled - either as independent contractors instead of employees or by assigning them to lower-risk classification codes to reduce insurance premiums [6][5].

"Misclassification is when a company says a worker is something they're not." - Hyring [6]

Some employers misclassify workers intentionally to save up to 30% on labor costs [6]. Others may do so unintentionally due to confusing classification rules. It’s estimated that 10% to 30% of U.S. employers misclassify at least some workers, leading to $22 billion in misclassified payroll annually [5]. Proper classification is essential - not just for compliance, but also to protect both company finances and employee benefits. Let’s take a closer look at the types of misclassification and how they affect businesses, particularly in the firearms industry.

One common type of misclassification involves treating employees as independent contractors. The key legal question here isn’t what the contract says, but the actual working relationship. Factors like who controls the worker’s schedule, provides equipment, or dictates work methods are what truly determine classification [3]. Even if a worker signs a 1099 agreement, they might still be considered an employee under the law.

Another type involves assigning incorrect workers' compensation class codes. These codes are tailored to specific industries and reflect the risk level of different roles [5]. For example, classifying a high-risk job under a low-risk code can significantly lower premiums. However, whether intentional or accidental, this practice can leave businesses exposed. As one insurance expert notes:

"A simple mistake can mean a costly audit" - JVRC Insurance [5]

The firearms industry provides clear examples of how misclassification occurs. Take a gunsmith, for example, who works regular hours in a shop. If they’re labeled as an independent contractor, despite the employer controlling their schedule and tools, they’re likely misclassified. Similarly, firearms instructors teaching scheduled classes may be treated as contractors when they’re functioning more like employees.

Class code errors are another issue. For instance, a business might classify a gunsmith or range safety officer under a low-risk administrative code rather than the correct high-risk category. While this might reduce premiums initially, it can lead to serious consequences. If an injury happens, the workers' compensation policy might not cover the claim, leaving the employer personally responsible for medical bills and legal costs [5].

Misclassifying workers can lead to serious financial and personal consequences. It impacts not only the businesses involved but also the workers themselves, creating a ripple effect across industries. Let’s break this down further.

Misclassification can be a costly mistake for businesses. If auditors uncover misclassified workers, companies might face retroactive premium charges ranging from 1% to 15% of their total payroll, depending on the industry [7]. These charges often cover several years of back-dated workers' compensation premiums, sometimes stretching over three years or more.

Beyond premium charges, misclassification can leave employers personally liable for medical expenses and wage replacement benefits if a worker gets injured. A notable example is FedEx Ground, which in 2015 paid a $228 million settlement in California after misclassifying thousands of delivery drivers as independent contractors. Despite requiring drivers to wear uniforms and follow strict schedules, the company denied them employee benefits and protections [7].

Businesses also risk hefty fines and legal costs. State penalties can range from $1,000 to $25,000 per worker, and audit or legal fees can climb to $15,000–$100,000 [7][8]. When combined with back taxes, unpaid overtime, and other legal expenses, the financial impact of misclassifying even one worker can easily reach six figures. Industries with higher risks, such as firearms businesses, face even steeper consequences. And these financial burdens don’t even account for how misclassification affects workers’ claims.

For workers, misclassification often means losing access to critical benefits. Insurance carriers frequently deny claims for those labeled as independent contractors, forcing individuals to pay out-of-pocket for medical expenses and miss out on wage replacement benefits during recovery [11].

In New Jersey’s trucking sector, misclassified workers lose an average of $26,253 annually in compensation and benefits compared to properly classified employees [11]. Across various fields, misclassified independent contractors can lose over $21,000 each year in wages and benefits [9].

"If you are misclassified as an independent contractor, you may be denied benefits and protections to which employees are legally entitled." - U.S. Department of Labor [10]

Workers can challenge their classification through state agencies to claim retroactive benefits, but this process is often time-consuming and requires extensive documentation or even legal help [10][11]. These individual losses also have broader implications, influencing industry-wide premium rates.

Misclassification doesn’t just harm individual businesses and workers - it drives up costs across entire industries. Employers who underreport payroll or assign incorrect class codes may initially save on premiums. However, when claims arise, insurers face unexpected losses that weren’t accounted for in the original premiums.

These losses force insurers to increase premiums across the board [5]. For example, the construction industry sees around $500 million in workers’ compensation premium adjustments annually due to misclassification [5].

"Misclassification also hurts law-abiding business owners who don't get to compete on a level playing field when some employers wrongly classify their workers as independent contractors and thereby lower their costs unlawfully." - U.S. Department of Labor [10]

Misclassifying employees doesn’t just hit businesses financially - it can also lead to severe legal consequences. These penalties, while varying by state, are designed to enforce compliance and can be devastating for companies that fail to follow the rules.

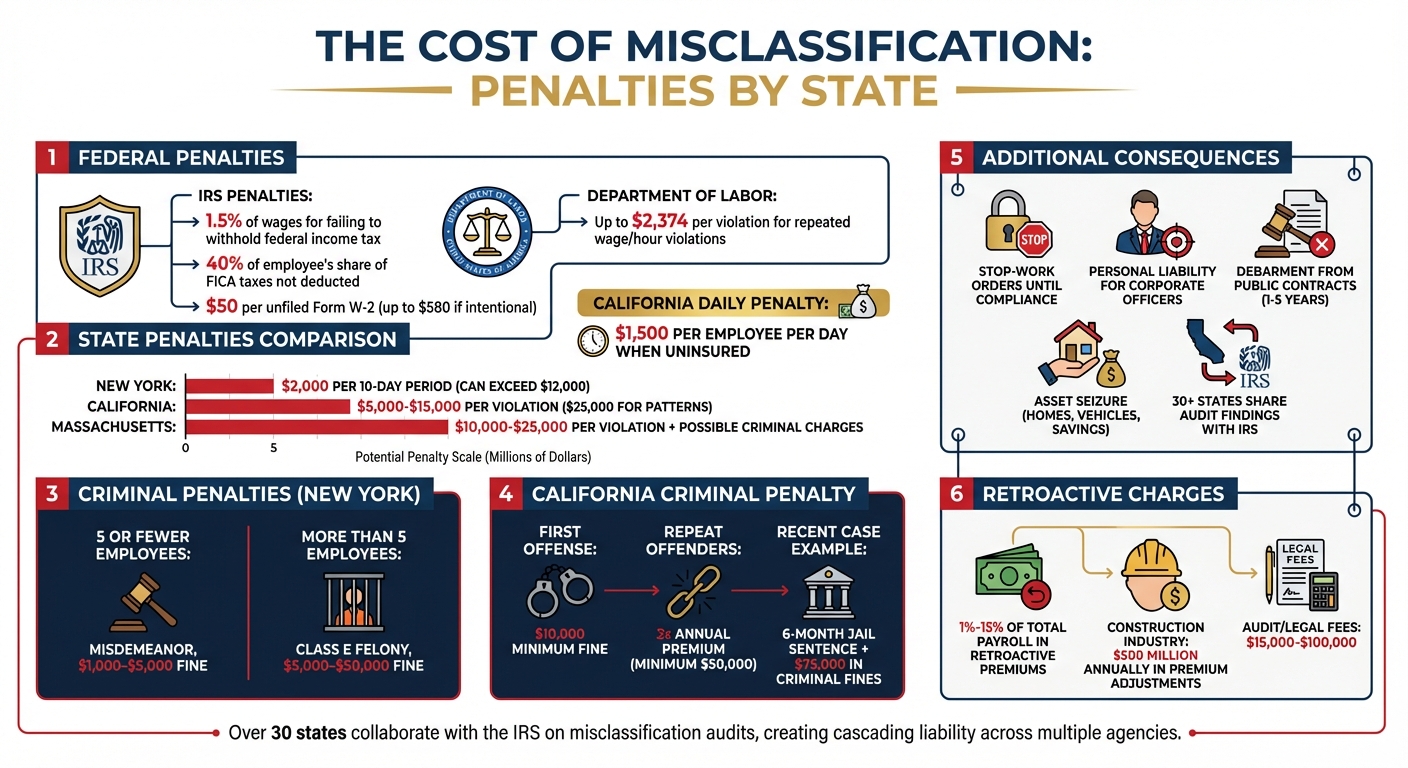

Legal penalties for misclassification can add up quickly. At the federal level, the IRS imposes 1.5% of wages for failing to withhold federal income tax and 40% of the employee's share of FICA taxes that weren’t deducted [7]. On top of that, the Department of Labor may levy civil penalties up to $2,374 per violation for repeated wage and hour violations [7]. The IRS also charges $50 per unfiled Form W-2, which can rise to $580 per form if the failure is deemed intentional [7].

State penalties, however, can be even harsher. For instance, in New York, businesses can face fines of $2,000 for every 10-day period they fail to provide coverage. By the time an employer receives notice, the penalty can easily exceed $12,000 [13]. California enforces civil penalties ranging from $5,000 to $15,000 per violation for intentional misclassification, and if a pattern is identified, this increases to $25,000 per violation [12][7]. Massachusetts takes it a step further, charging between $10,000 and $25,000 per violation, with the possibility of criminal charges [7].

Businesses also risk stop-work orders, which halt operations until workers' compensation insurance is secured and fines are paid [14][16]. In California, the daily penalty for being uninsured is $1,500 per employee, and personal assets like homes and savings accounts can be seized to cover unpaid obligations [16].

"California law pierces the corporate veil for workers' compensation violations, making owners personally responsible... Home, vehicles, savings accounts [are at risk]." - Josh Cotner, CEO, Contractors Choice Agency [16]

These financial penalties often serve as a prelude to even more serious criminal repercussions.

Many states have taken penalties a step further by imposing criminal sanctions for intentional misclassification. In New York, the severity of the punishment depends on the number of employees affected. For five or fewer employees, failure to secure workers' compensation coverage is classified as a misdemeanor, carrying fines of $1,000 to $5,000. For more than five employees, it escalates to a Class E felony, with fines ranging from $5,000 to $50,000 [13].

"Failure to secure workers' compensation coverage for more than five employees within a 12-month period is a class E felony punishable by a fine of between $5,000 and $50,000." - New York State Workers' Compensation Board [14]

California enforces even stricter penalties, including jail time. A first offense comes with a minimum $10,000 fine, while repeat offenders face fines equal to three times the annual premium, with a minimum penalty of $50,000 [16]. In one recent case, a contractor in Fresno, California, received a six-month jail sentence and was ordered to pay $75,000 in criminal fines, which was triple his estimated annual premium, after a second offense [16].

Beyond fines and imprisonment, misclassification convictions can also result in debarment from public contracts. In states like New York, businesses found guilty of non-compliance are barred from bidding on public works projects for one to five years [14][15]. Additionally, corporate officers such as the President, Secretary, and Treasurer can be held personally liable for failing to secure workers' compensation insurance [14].

To make matters worse, over 30 states now collaborate with the IRS to share audit findings related to misclassification. This "cascading liability" means that a single misclassification audit can trigger investigations and penalties from multiple agencies simultaneously [7]. Such coordination amplifies the risks, leaving businesses vulnerable to overlapping penalties from both state and federal authorities.

Getting employee classification right is key to avoiding penalties and ensuring proper worker coverage. It involves understanding specific criteria, conducting regular reviews, and working with insurance providers familiar with the firearms industry.

The first step is determining whether a worker is genuinely independent or economically reliant on your business. The Control Test evaluates if the worker operates free from your control or direction - both as stated in contracts and in daily practice [17]. This test digs deeper than just paperwork, focusing on the actual working relationship.

Similarly, the Independent Business Test ensures contractors are running their own trade, occupation, or business [17]. Proper classification here can help you avoid the financial and legal risks mentioned earlier.

For firearms businesses, classification can be even more specific. Workers might be grouped based on their level of access to inventory. For example, those with "direct access" handle firearms, while those with "constructive access" manage security or inventory [18]. Additionally, some states, like Pennsylvania, require a written contract for a worker to qualify as an independent contractor in certain industries [17].

When assigning workers' compensation class codes, focus on your business's main operations rather than trying to classify each individual job. For instance, the Clerical Office Employees code (8810) applies only to staff who spend all their time on administrative tasks in an office. If they occasionally assist in retail or warehouse areas, their payroll should be allocated to the higher-rated governing code for your business.

Similarly, firearms businesses that own their inventory should be classified under Wholesale (Code 8018) rather than Storage Warehouse (Code 8292), which is reserved for third-party logistics providers. Misclassification can lead to costly premium adjustments during audits. Regular audits help ensure these classifications remain accurate.

Routine audits are essential. For example, a small ELA Practice firm avoided almost $300,000 in penalties during an October 2025 review by reclassifying workers, updating contracts, and implementing a compliant payroll system [4]. This proactive approach saved them from back taxes, unpaid benefits, and fines.

Annual reviews using the IRS Three-Category Test - which examines work control, financial oversight, and relationship permanence - are a good practice [4][19]. These reviews ensure compliance with IRS and Department of Labor standards.

Firearms businesses should also update their background screening and classification policies annually to reflect changes in federal, state, or local laws [18]. A written policy requiring employees to report changes in their eligibility to handle firearms within 24 hours is another smart move [18].

Regular audits not only keep workers' compensation class codes and payroll projections accurate but also help avoid premium hikes. With $22 billion in payroll misclassified each year - 12% of it in California alone - these reviews can save businesses from hefty retroactive charges [5].

Internal audits are important, but partnering with insurance providers who understand the firearms industry adds another layer of protection. These providers, like Joseph Chiarello & Co., Inc., specialize in preventing audit surprises by helping businesses classify employees correctly from the start. They offer tools like the NCCI class look-up and direct underwriting support to resolve any classification uncertainties.

"Promote a safe work environment by doing a background check for your new hires. We offer a background check package that will reveal the quality of every applicant." – Joseph Chiarello & Co., Inc. [18]

Specialized insurers also provide loss control consulting, identifying risks unique to gun shops, manufacturers, and shooting ranges. Accurate classification and screening can lead to better insurance terms, lower premiums, and broader coverage for Workers' Compensation and Commercial General Liability [18].

For firearms businesses, investing in proper screening is both affordable and effective. Background check packages through providers like IntelliCorp start at just $16.45 per applicant [18]. This small investment ensures compliance and protects your workers while building trust with regulators and insurers.

Firearms businesses operate in a highly regulated environment, facing unique challenges that standard insurance policies often fail to address. One misstep, such as an IRS finding, can set off a chain reaction of liabilities involving multiple agencies[7]. To navigate these risks, specialized insurance solutions are essential.

Joseph Chiarello & Co., Inc. offers workers' compensation coverage specifically designed for the firearms industry. Their services go beyond basic coverage by providing loss control measures tailored to the unique risks found in gun shops, manufacturing facilities, and shooting ranges. These measures aim to reduce workplace injuries and minimize claims.

One standout feature is their background check packages, which help firearms businesses vet employees thoroughly from the outset. This proactive approach addresses potential misclassification issues before they escalate into costly audits. For instance, having more than 30% of your workforce classified as contractors is a major red flag for IRS audits[7]. The company ensures proper worker classification by focusing on the "economic reality" of the relationship between the worker and the business, rather than just relying on contractual labels[10]. These specialized services provide a solid foundation for compliance and operational security.

Industry-specific insurance programs offer firearms businesses a way to manage financial risks tied to worker misclassification. Proper classification ensures that employees receive critical protections, such as medical benefits and wage replacement, while also promoting fair competition by preventing cost-cutting through misclassification[10].

State workers' compensation boards often have their own criteria for determining employment status, which may not align with IRS or federal definitions. Specialized providers are well-versed in these differences and help businesses navigate the intricate regulatory framework. With federal and state governments losing billions annually due to worker misclassification, enforcement efforts are ramping up[10]. Tailored insurance programs not only help businesses maintain compliance but also protect employees and safeguard the company’s financial health.

Misclassifying employees as independent contractors isn’t just a paperwork mistake - it can deprive workers of critical benefits. The U.S. Department of Labor emphasizes the seriousness of this issue:

"Misclassifying employees as independent contractors is a serious problem because misclassified employees may not receive the minimum wage and overtime pay to which they are entitled under the FLSA or other benefits and protections to which they are entitled under the law." [2]

While treating workers as contractors might initially cut labor costs by 20%–40%, those savings often vanish under the weight of penalties, back taxes, and legal fees [4]. For instance, in California, willful misclassification can lead to steep civil penalties and escalating fines [1]. One Virginia construction firm learned this the hard way, paying over $1.1 million in back wages and liquidated damages for misclassifying workers [4].

For firearms businesses, the stakes are even higher. Beyond financial penalties, misclassification could result in IRS audits, state enforcement actions, or even the loss of a business license. With both federal and state agencies increasing enforcement efforts, getting worker classification right is crucial - not just for compliance but for long-term business stability.

To avoid these risks, companies should prioritize regular classification audits. Tools like the IRS Three-Category test or the DOL Economic Reality test can help ensure accuracy. Formalized written agreements are also key, and when uncertainty arises, it’s safer to classify workers as employees. Employment law expert John Rabil puts it plainly:

"When in doubt, it makes sense to classify conservatively. You aren't going to misclassify someone as an employee." [4]

Taking proactive steps not only shields businesses from legal trouble but also safeguards workers and strengthens financial stability.

To figure out whether a 1099 worker should actually be classified as an employee, take a close look at how much control you have over their work. If you dictate how, when, and where tasks are carried out, it’s a strong sign they might be an employee rather than an independent contractor.

Legal guidelines, like those focusing on behavioral and financial control, can help clarify their status. Misclassifying workers isn’t just a paperwork issue - it can lead to serious problems, such as denied workers’ compensation claims and hefty penalties. That’s why it’s important to perform regular compliance checks to avoid these risks.

If a worker is misclassified, their workers’ compensation claim could be denied or reduced. This means they may miss out on benefits and financial compensation that they would normally be entitled to as an employee. For employers, misclassification can also create serious compliance problems, potentially leading to legal and financial consequences.

Firearms businesses need to carefully evaluate how they classify their workers - whether as employees or independent contractors. For example, in states like California, the ABC test is commonly used to determine worker classification. Ensuring compliance with these guidelines is essential to avoid potential legal and financial repercussions. Misclassifying workers can result in penalties, so addressing this issue thoroughly from the start is a smart move.

Don't wait until it's too late to make sure your gun shop is covered. At Joseph Chiarello & Co., Inc., we’re here to help you navigate the ins and outs of gun shop workers compensation insurance to ensure you're prepared for any noise-related risks, including hearing damage. Reach out to us today to review your current policy or get a customized quote. Protect your team and your business with the right coverage—because their safety is worth it.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!